A person’s gross all out income is the aggregate of income under five distinct heads determined dependent on the tax laws. One of these heads is ‘income from house property’. This head incorporates lease earned from building or land appurtenant thereto which is chargeable to tax.

Income is taxable under the head house property if conditions to Section 22 are fulfilled. According to this segment, to get income taxed under the head house property, the assessee must be the proprietor of the property and income must be gotten from building or land appurtenant thereto. Be that as it may, on the off chance that it’s utilized for assessee’s own business, at that point, it won’t be taxable under the head house property.

To ascertain tax under the head house property, we first need to see if the house is self-involved or let out or to be treated as considered to be let out. This order is an absolute necessity as figuring of taxable income under the head house property depends on it. In this article, we will talk about how to compute taxable income under the head house property when the house is self-involved.

What is a self-involved house property

According to the income tax act, self-involved house property is the one which is utilized for assessee’s own living arrangement. It will likewise be treated as self-involved if it is utilized for the private motivation behind guardians, companion or youngsters.

According to the arrangements, on the off chance that more than one house is self-involved by the assessee, at that point, just one as per the decision of the assessee will be considered as self-involved and all others will be considered as regarded to be let out. From money related the year 2019-20 forward, the advantage of considering the houses as self-involved has been stretched out to 2 houses. Along these lines, for income tax purposes, from money related the year 2019-20 ahead, you can consider 2 houses as self-involved and staying as let-out.

If it’s not too much trouble note, if the property is utilized for own business or calling, income from such property isn’t chargeable to tax under the head house property.

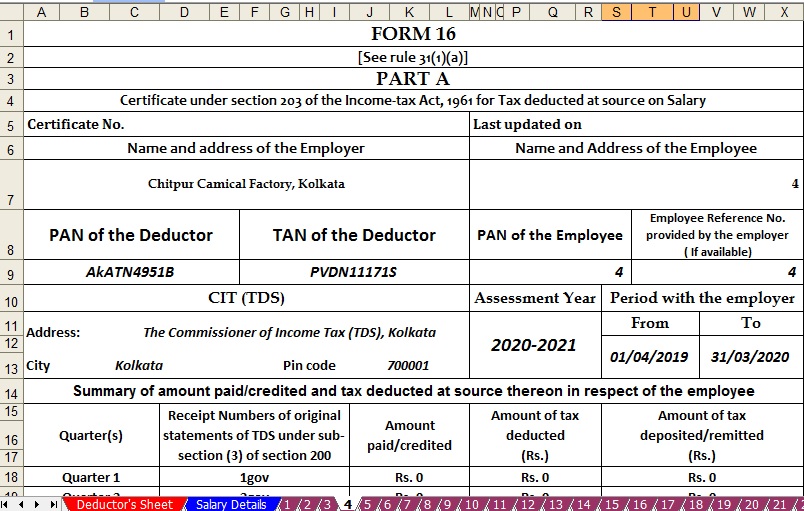

Download Automated Excel Based Master of Revised Form 16 Part A&B for the Financial The Year 2019-20 [This Excel Utility can prepare at a time 100 Employees Revised Form 16 Part A&B ]

Steps to ascertain income from house property

Here are simply the means to ascertain income from a self involved house property.

1. Determine gross yearly worth

2. From stage 1 deduct city tax paid by the proprietor during the earlier year to discover the net yearly worth

3. From the net yearly worth deduct tax derivation under segment 24 to get income from house property.

In the event that the house is completely self-involved for the entire earlier year and no other advantage is gotten from it, at that point net yearly worth ought to be considered as Nil. This implies you need not compute stage 1 and 2 as talked about above.

Yearly estimation of the property will not be considered as nil if such house or some portion of it is really let out during the entire or any piece of the earlier year or some other advantage is gotten from it.

At the point when the assessee self-involved more than one house property

On the off chance that assessee self-involved more than one house, at that point he may practice a choice to get anyone act naturally involved. From the money related year, 2019-20 ahead assessee has the choice to choose any two houses as self-involved.

The yearly estimation of the house chose by the assessee as self-involved will be considered as nil. Every other house will be considered as regarded to be let out. Such choice of choosing a house as self-involved for income tax estimation can be changed each year dependent on assessee’s decision.

Tax conclusion under Section 24

As talked about in our previous article, standard derivation under area 24 will be constantly considered as zero for house property which is considered as self-involved as its yearly worth is nil. In any case, the assessee will be qualified for a tax derivation on enthusiasm on acquired capital.

On the off chance that assessee has obtained or developed the property with capital acquired on or after 1.4.1999 and such procurement or development is finished inside a time of 5 years from the finish of the money related year in which the capital is obtained, at that point enthusiasm on acquired capital or Rs 2,00,000, whichever is lower will be permitted as a tax conclusion under area 24.

In some other case, tax reasoning on enthusiasm on acquired capital is accessible up to the greatest constraint of Rs 30,000. This implies enthusiasm on obtained capital or Rs 30,000 whichever is lower will be permitted as a finding.

If there should be an occurrence of a joint home advance, both will be independently qualified for area 24 reasoning. For this situation Rs 2,00,000 and Rs 30, 000 as the case might be will be permitted as most extreme restriction of tax reasoning for the two people independently. This implies, in the event that you alongside your mate taken a joint home advance in the extent of 50:50, at that point, both of you can guarantee up to a most extreme restriction of Rs 1,50,000 each (in all-out Rs 300000) u/s 80C for head installments and up to Rs 2,00,000 or Rs 30,000 each (in absolute Rs 4,00,000 or Rs 60,000) as the case might be for enthusiasm on obtained capital under area 24 as tax derivations.

To get the finding of enthusiasm on acquired capital, the assessee needs to get a testament from the person to whom such intrigue is payable.

Download Automated Excel Based Master of Revised Form 16 Part B for the Financial Year2019-20 [This Excel Utility can prepare at a time 100 Employees Revised Form 16 Part B ]

Income Tax Revised Form 16 Part B

Where the house property is self involved for part of the year

On the off chance that the house property is self-involved for part of the year and let out the other piece of the year, at that point the yearly estimation of such property is to be determined as though its let out for the entire year. In such a case, the time of self-involved is unessential. This implies the property will be treated as self-involved house property if it is not let out in any event, for a solitary day during the earlier year.

While ascertaining yearly estimation of the property, the normal lease as in segment 23(1)(a), will be taken for the entire year however the real lease got or receivable will be taken uniquely for the let-out period.

Format to calculate income

| Sr. No. | Particulars | Amount in Rupees |

| 1. | Gross Annual Value | Nil |

| 2. | Less: Municipal taxes paid during the year | Nil |

| 3. | Net Annual Value (1-2) | Nil |

| 4. | Less: Deduction under section 24 | |

| 4.1 | Standard deduction U/s 24 (30% on Sr. No. 3) | Nil |

| 4.2 | Interest on borrowed capital | (XXX) |

| 5 | Income from house property (Sr. No. 3- Sr. No. 4) | (XXX) |

From the above calculation position, it tends to be seen that for self-involved house property, income will consistently be nil or negative depending on the intrigue payable on obtained capital. Anyway, loss can’t surpass Rs 2, 00,000 or Rs 30,000 by and large.

Loss from house property

Loss from one house property can be set off against income from other house property for the equivalent money related year. In the event that it’s not adequate to set off the entire loss, at that point the unadjusted loss is permitted to be set off from income chargeable under the head pay rates, business or calling, capital additions or different sources subject to a greatest restriction of Rs 2,00,000. On the off chance that any unclaimed loss forgot about, at that point, it very well may be conveyed forward to resulting years to change it against income from house property.