Tax benefits to the Senior Citizen as per Income Tax Act | These articles discuss the income tax

benefits available to senior citizens. A person becomes old under the Income Tax Act after completing

60 years or at least one day. After he reaches the age of 60, old age status gives him relief in that

financial year. There are few income tax benefits for the Sr.Citizen.

They are listed below:

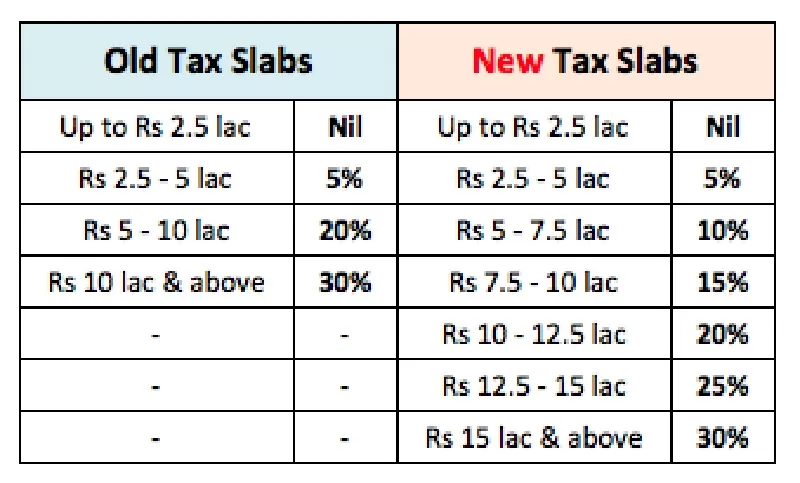

The Sr. Citizens between the ages of 60 to 80 Years and Very senior citizens above 80 Years are granted higher deduction limits than regular taxpayers. The exemption threshold is the amount of tax-free income. The exemption limits for seniors and very seniors for the fiscal year 2023-24 are as follows:

- An elderly Very elderly person is assigned a higher exclusion limit compared to non-elderly persons. The exemption limit for senior citizens for the financial year 2023-24 is Rs. 3,00,0 The deduction limit for senior non-citizens is Rs. 2,50,0 So, it can be seen that the additional amount is Rs 50,000/-. An additional exemption limit in the form of 50,000 is available for elderly residents compared to regular taxpayers in the basic income tax slab.

- An elderly person is given more limited deductions than others. The deduction limit for the fiscal year 2023-24 is for a resident elderly person. 5,00,0 The deduction limit for senior non-citizens is Rs. 2,50,0 So, it can be seen that the additional amount is Rs. 2,50,000 in the form of a maximum exemption limit of 50 for a much older person as compared to ordinary taxpayers.

- Before understanding the age criteria, it is very important to note that the tax exemptions granted to the elderly/very old under the Income Tax Act are very large for the elderly and residents. In other words, these benefits are not available to a non-resident even at an advanced age. The age and other criteria for being old age and super senior under the Income Tax Act are as follows:

- Seniority Criteria The criteria for the most elderly are being aged 60 years or over but less than 80 years at any time during the relevant year.

- Must be 80 years of age or older at any time during the relevant year. Must be a resident must be a resident

- The income tax bill effectively protects the country’s elderly by providing more tax benefits. In this section, you can learn about the various benefits that the Income Tax Act provides to senior citizens

- Under Section 208, the estimated tax for the year is Rs. 10,000 or more, the tax must be paid in advance in the form of “advance tax”. However, Section 207 exempts an elderly resident from payment of advance tax. Under Section 207, an elderly resident (that is, a person aged 60 years or older in the relevant financial year) who has no income from trade or occupation is not liable to pay advance tax

- Section 80TTB of the Income Tax Act makes provisions relating to the tax relief available to banks, post offices, or cooperative banks on account of income interest accrued up to Rs.50,000. 50,000 to an elderly person (i.e., an individual aged 60 years or above). Interest earned on savings deposits and principal deposits are both eligible for deduction under this provision.

- Section 194A of the Income Tax Act provides that no tax shall be levied by a bank or post office or cooperative bank on payment of interest up to Rs.50,000 to a senior citizen. 50,000. Therefore, the limit should be calculated separately for each bank.

- Section 80DDB of the Income Tax Act provides for various provisions relating to tax deductions in respect of medical expenses. Click on the link below Section 80DDB which contains details of special exemptions under Section 80DDB for an elderly person.

- Section 80D of the Income Tax Act taxes health insurance and b other expenses various provisions are given in relation to llamas.

- The Income Tax Act, 1961 does not exempt an old or very old person from filing a return. However, the Finance Act, 2021 has introduced a new section 194P to provide relief to senior citizens (those aged 75 years or above) and reduce their burden.

- This bill requires a bank to deduct tax under this bill if it has an account that receives pension income. If a payer is a resident person, aged 75 or over, at any time during the year and the following conditions are met, the tax will be collected under this new law:

(a) The beneficiary’s gross income is in the form of retirement pensions and any income received or to be received from any account maintained by the drawer. And

(b) The receiver files a return with the deductor containing the prescribed specification.

If tax is paid on the income of such an elderly person, he or she is not liable to refund the income for the previous tax year.